A breakdown of what living paycheck to paycheck looks like

Also, 80 percent would be of the daily workforce, not those who are retired on pensions or those on some form of welfare. What government agency or otherwise provided the 80 percent number?

Clearly, I’m skeptical of such an amazingly high figure. If this is correct, I expect to soon see mass starvation and rioting in the streets since we have now seen 40 percent file for unemployment.

A: We have received a number of letters and emails like yours wondering whether the financial crisis is real and how people are surviving during this unprecedented time. Even if you have a job with health insurance and enough money to buy what you need and put food on the table, it’s difficult to imagine not being able to empathize with something as devastating as the covid-19 pandemic.

And yet, our mail shows that some people simply don’t believe that so many people are a paycheck away from not having enough money to pay their bills. So, here’s a rundown of what we’re seeing.

There are millions of Americans living paycheck to paycheck in this country, as many surveys have shown. According to Nielsen data, the American Payroll Association, CareerBuilder and the National Endowment for Financial Education, somewhere between 50 percent and 78 percent of employees earn just enough money to pay their bills each month. Should they miss a paycheck, some of those bills would go unpaid.

In addition, almost 3 in 10 adults have no emergency savings at all, according to Bankrate’s July 2019 Financial Security Index, while the January 2020 Financial Security Index survey showed that 4 in 10 U.S. adults would cover the cost of a $1,000 car repair or emergency room visit using savings; Nielsen data from 2015 showed that nearly 25 percent of families earning $150,000 a year or more lived paycheck to paycheck; and a Gallup poll released in December found that a record 33 percent of Americans say they or a family member put off treatment for a medical condition in the past year because of cost. A quarter of Americans say their untreated medical condition was serious.

In a 2019 report on the economic well-being of U.S. households, the Federal Reserve Bank determined that nearly 40 percent of U.S. adults wouldn’t be able to cover a $400 emergency with cash, savings or a credit card charge that they could quickly pay off. (This spring, Federal Reserve Chair Jerome H. Powell said that 40 percent of households earning $40,000 or less had lost income because of the pandemic, increasing financial stress and pressure.)

All of these studies, by the way, were done before the coronavirus pandemic, which has done nothing to ease the financial pressures so many Americans are facing and in fact has exacerbated them tremendously.

So let’s talk about the effect of covid-19 on the unemployment rate. To date, roughly 32 million Americans have filed for some sort of unemployment assistance. This has happened over the past 19 weeks, where the number of first-time unemployment claims has exceeded 1 million per week, an unprecedented number in U.S. history.

As of July 30, the Federal Reserve Bank of St. Louis reported there were more than 17 million continuing claims, an uptick from the prior week and a higher number than just about anything in the modern era.

Also, according to the Federal Reserve Bank of St. Louis, the monthly unemployment rate is 11.1 percent, as of July 2. The Federal Reserve Bank of Chicago does a slightly different calculation, and after the release of the latest current population survey estimates and other micro data, believes that the total unemployment rate as of mid-May was about 27.6 percent.

These numbers are very high, but we couldn’t find evidence that the number of unemployed had reached the 40 percent number you cite.

Since the beginning of the covid-19 pandemic recession, we have seen unprecedented support provided by Congress to the American public in the way of a $1,200 payment to nearly 90 million Americans, plus a dramatic expansion of unemployment benefits, including an extra $600 per week on top of regular unemployment benefits, which were then extended by 13 weeks in the Cares Act, and the ability for part-time and self-employed people (who normally can’t apply for unemployment assistance) to apply for pandemic unemployment assistance, known as PUA.

The Paycheck Protection Program allowed thousands of employers to keep most or all of their employees on payroll through the spring. There are thousands of other programs providing financial support on a state and local level, as well.

Despite this, it’s clear that many of our fellow citizens are suffering. We have seen equally unprecedented lines at food banks across the country, some stretching for miles. The food bank at which we volunteer, which is at a community center in Highwood, Ill., used to serve 150 families every other week and still have some food left over to donate to the church’s food pantry next door. Today, the food bank serves more than 375 families every week, with almost nothing left.

New surveys have determined that the level of hunger, which is typically known as food insecurity, is rising dramatically. According to the Brookings Institution: “By the end of April, more than one in five households in the United States, and two in five households with mothers with children 12 and under, were food insecure. In almost one in five households of mothers with children age 12 and under, the children were experiencing food insecurity.”

As for rioting in the streets, the pictures online and on television speak for themselves.

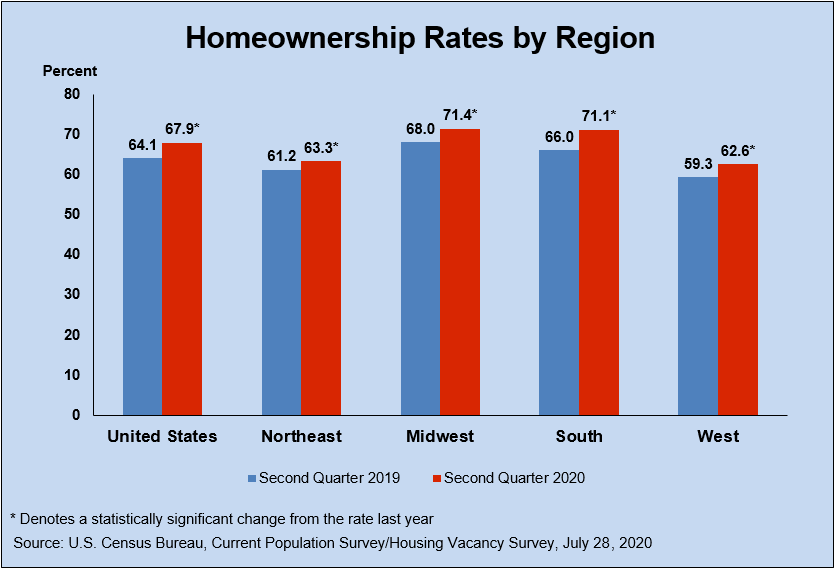

From a housing perspective, there has been a dramatic uptick in the level of homeownership over the past year, from 64.1 percent in 2019 to nearly 67.9 percent this year, according to the Census Bureau’s second-quarter 2020 report on Residential Vacancies and Homeownership.

Interest rates have fallen to an all-time low during the pandemic, and the Federal Reserve Bank has indicated it will keep the federal funds rate at a target of 0 percent to 0.25 percent for the foreseeable future.

Here’s the question economists are asking: How many people will lose their home once the financial support from the government stops? The $600 per week in extra support is ending and may be replaced by a smaller amount or eliminated entirely. There was no indication at press time that the federal student loan forbearance (scheduled to end Sept. 30) or the eviction moratorium will be continued. But there is talk about providing huge financial support to landlords and commercial property owners, who would lose their properties to the bank because their tenants haven’t paid them rent.

Economists talk about a cash cliff. Well, here we are, and the abyss looks pretty scary.

Read more:

{kind=link}